Welcome to Part 2 of our ongoing series on personal financial statements. If you have read the first part of this series you should now have a solid understanding of what an income statement is, how it is created and how it can benefit you.

In this article, we will move on to the second financial statement, the balance sheet. Since the balance sheet and the income statement are inextricably linked, I highly recommend checking out the first part of this series before continuing with part two.

To thoroughly demonstrate the workings of a personal balance sheet, we will once again join our trusted sales executive Aiman, as he makes his journey towards financial awareness. Previously, Aiman had calculated his net result through the creation of a personal income statement.

Since that time, a lot has happened in Aiman’s life. He had to break up with his girlfriend (for obvious reasons) and has since been enjoying the single life. He has been tightly controlling his spending and calculates monthly income statements at the end of each month. Aiman is still curious about his financial situation and wants to see if this frugal lifestyle has actually had an effect on his financial standing. A perfect tool for this is a personal balance sheet. Let’s get started!

The function of a balance sheet is to present a snapshot of your financial position at any given time. The key here is snapshot. Where the Income Statement presents your net result over a given period (month, quarter, year), the balance only shows you a single moment in time.

As probably the most well-known of all the financial statements, the name balance sheet already gives you some indication as to what the statement looks like. A balance sheet, unsurprisingly, has to balance. It shows you:

- Your Assets (what you have spent money on)

- Your Liabilities (how you obtained said money)

- Your Net worth (Assets – Liabilities)

Balance in all things

The Balance Sheet concept is widely used by people, businesses and countries. For people, it can be used as a quick way to calculate your net worth. For businesses, the balance sheet shows the assets and liabilities of the company, with the difference being shareholder’s equity. Shareholder’s equity is the business equivalent of net worth.

Although countries generally don’t publish complete balance sheets, they do use the balancing concept when calculating their investment position. External assets and external liabilities are balanced with the difference being the net investment position.

The concept is also used in the Balance of Payments, which is basically the countries’ cash flow statement. Outgoing streams of goods, services and money are balanced against incoming streams to calculate the countries’ trade surplus or deficit.

As you can see, the balance sheet concept can be applied to anything, as long as it has an economic function. You can even make a balance sheet for your entire family or for you and your partner.

The balance sheet explained

The reason that the balance sheet has to balance is that every asset you own has to have been paid for in one way or another. For example, you might pay for your house with a mortgage, for your food with credit-card debt, and for a new car with money that you earned yourself. Each of these economic actions has a double consequence in your balance sheet. If you take out a mortgage and buy a house, you would gain an asset (the house) and a liability (the mortgage). Both sides of the balance sheet would change, but the balance would remain intact. This even applies to assets you obtain for free. Let’s say that your brother gave you a new car for your birthday. You don’t offer up an equally large asset (money) and you don’t go into debt, so how does the balance sheet remain balanced? Let’s rewrite the formula to see how this makes sense:

Assets – liabilities = Net worth -> Liabilities + Net worth = Assets

If you look at it this way, all your assets have been financed by either liabilities or net worth. If you obtain a new asset (car) without a decrease in another asset (money) or an increase in a liability (debt) the increase adds to your net worth. So if you get a car for free, that would mean a direct increase in your net worth!

To show you how a balance sheet works in practice, let’s join Aiman when he calculates his balance sheet for the end of February 2017.

He first makes a list of his assets. This includes his retirement savings, his current checking and savings account balances, any bonds he might have, the total value of any stock holdings he might have, his home, and his automobiles.

He can also include smaller things like clothes, phones and furniture but that depends on how precise he wants to get. Subscriptions such as gym memberships and advanced insurance payments should also be listed as assets. Think about it, if he has paid for something that he has not used yet (to its fullest) the remaining value of these subscriptions is still of value to him, so, therefore, he can record them as assets.

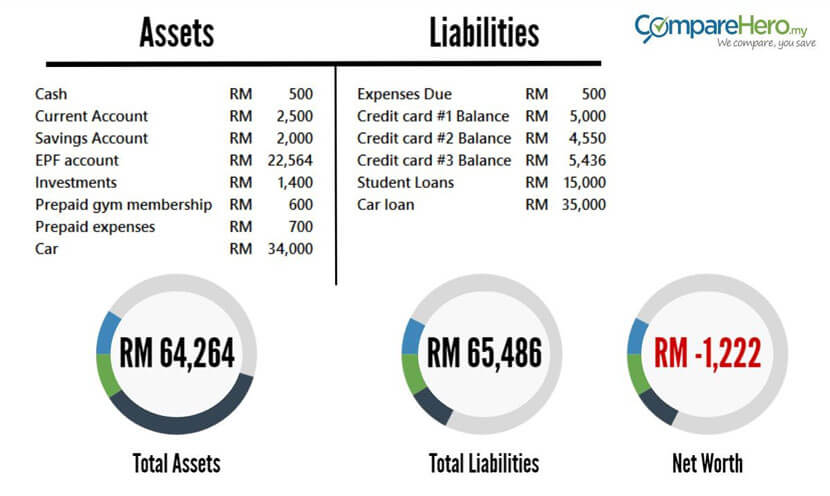

- RM500 in cash

- RM4,500 in his current account

- RM4,000 in his savings account

- He EPF retirement account currently contains RM22,564

- His current combined investments are worth RM1,400

- He previously paid RM720 for a 6-month gym membership of which he still has 5 months remaining (720 – (720 / 6 )) = RM600

- Similar to the Gym membership he prepaid for various other expenses with a combined worth of RM700

- He recently bought a new car, which has a current resale value of RM34,000

His combined assets have a total value of RM64,264

Then, he lists all his liabilities. He should list all of his credit card balances, personal loans, student loans, car loans and mortgages. Bills that he has not paid yet should also be recorded as liabilities because he is effectively indebted to the other party.

- He has 3 credit cards, with a combined outstanding balance of RM14,986

- He has student loans remaining worth RM15,000

- He financed his car with a car loan worth RM35,000

- He still has bills outstanding with a combined worth of RM500, he records these as a liability account called ‘Expenses Due’

His combined liabilities have a total value of RM65,486

Lastly, he is able to calculate his Net-worth:

Total Assets (RM64,264) – Total Liabilities (RM65,486) = Net Worth (RM -1,222)

Let’s put everything together to get a complete view:

A negative net worth spells trouble

That does not look very promising! Even though Aiman has been very conservative with his spending over the last months, his balance shows a negative net worth. If Aiman sold all his assets to pay off all his debt, he would still end up in the red. However, as long as Aiman is running a positive net result on his income statement, his net worth should increase every month.

To turn things around, if Aiman could consistently run a positive net result of RM400 a month, he will most likely turn his net worth positive in the next 4 months. That is an exciting prospect! Although turning your net worth positive is not likely to have any immediate effects, it is your first step towards financial freedom.

Out of balance?

So how do you know if you have listed everything correctly? In the case of personal balance sheets, your net worth is the plug figure that bridges the gap between your assets and liabilities. Once you have created your first balance sheet and you are using monthly income statements, the change in your net worth should always correspond with your net result for the month. If there is a big difference between the two, then most likely you have made a mistake somewhere.

Your Net Worth is important

Among other factors, your net worth actually plays quite a large role in determining your credit rating. Although most banks keep their rating algorithms a secret, they most likely calculate some version of your net worth and compare that to your total debt. The ratio at which your net worth compares to your debt is called your financial leverage. Financial leverage is a ratio that measures how much of your assets have been financed with debt. Your financial leverage gives your bank a strong indicator of how risky it is to provide you with extra lines of credit. If you want to know more about your credit rating, go here.

A good way to track your net worth is to calculate your personal balance sheet every six months. Don’t be alarmed if your net worth turns out to be negative. Especially if you are still studying or just started working, your net worth will most likely be negative. What matters is that you consistently try to improve your net worth! To get you started we’ve listed the best ways to increase your net worth:

Cut your spending

Are you surprised? No matter how many budgets and financial tools you use, if you are spending more than you earn, you will lose money. You can use the monthly income statements described in the previous article to check if you are on track with your spending. As a general rule you can assume that if your net result for the month is positive, your net worth will increase.

Buy income generating assets

Income generating assets are assets that help you to increase your income. Most of the times these are investments that generate a passive income through either dividends, interest or rent.

You can obtain dividends through business ownership. There are a lot of businesses out there who reliably pay out dividends each year. It’s a little riskier than a savings account but the returns are generally higher. To reduce the risk you could also invest in a mutual fund that focuses on low-risk dividend stocks. The added diversification will protect you against any market downturns.

You can earn interest through lending. The most common way that you can enter the debt market is through bonds. Bonds are essentially interest bearing loans that you can make to companies. Bonds are generally safer than stocks in terms of risk.

You can earn rent by renting out property. This can be as basic as making an Airbnb listing for your spare room or investing in a community real estate fund. Real Estate can be a reliable source of passive income, but to benefit you generally need a large capital investment.

And lastly, the most important income generating asset that you have. Yourself! You can increase your earning potential by educating yourself. Get additional degrees, follow online seminars and workshops. Get more experience or become more specialised in your particular field. There are tons of ways in which you can increase your income potential. As always, use your best judgment, and don’t fall for one of the many online scams that try to sell you expensive education seminars. We’ve listed the most common online scams in Malaysia for you here.

Reduce interest bearing liabilities

Your monthly interest payments may not seem like much, but in aggregate they are eating up your hard earned money. That’s money you could have used to buy more assets or make larger repayments. If you can, try repaying more than the minimum required repayment on your credit card debt. You should minimise your total interest-bearing debt as much as possible.

It might even be beneficial for you apply for a balance transfer card with a lower interest rate. Essentially, a balance transfer card allows you to pay off one credit card with another credit card with a lower interest rate, for a more thorough explanation, go here. Be careful with this, though, the added transfer rate and upfront rates can be misleading. However, if you pay attention the balance transfer card can be a quick way to reduce your interest payments. To make it easy for you, we’ve listed a couple of the best balance transfer cards for you here.

The final balance

Making substantial increases in your net worth is not a short time pursuit. Like most important things, it requires effort and commitment. The first step is to create awareness. If you have been following the examples provided in this article, you should be relatively comfortable making your personal balance sheet and calculating your net worth. We have given you some options as to how you can increase your net worth, the rest is up to you.

In the next part of this series, we will take a closer look at your cash-flow and show you how to construct your personal cash-flow statement. Stay tuned!

Download the Balance Sheet Template

To help get you started, use our downloadable Balance Sheet Statement template and key in your assets and liabilities! The sheet will auto-calculate your net worth and help get you on your way to budgeting your finances. Download Balance Sheet Template.

|

|

About the writer

About the writer

Jesse is a Guest Writer at CompareHero.my. A business student with a passion for finance and football, he is interested in new cultures and stepping out of his comfort zone.

CompareHero.my strives to empower Malaysians with financial literacy and the tools to make better financial decisions in life. Find and compare the best credit cards, and personal loans on CompareHero.my today.

Back to Blog

Back to Blog